Age Pension and super: What changes at 67?

, Your retirement

In most areas of life, planning ahead achieves three positive outcomes by:

But we’re not all the same. The Retirement Essentials team likes to compare the idea of retirement planning to that of travel. Let’s say there is a lot of money at stake. In retirement, there is; your super and how you use it, as well as an Age Pension entitlement. So, we’ll use the analogy of a six-week trip to Europe. Different people will approach this trip in different ways.

Many will book a fully guided tour which includes prebooked airfares, accommodation and activities. It’s fair to call that a low-risk option. Others will prefer a DIY approach, securing accommodation with Air BnB or Booking.com, buying their own airfares and undertaking lots of research to plan how they will spend their time while away. It’s a more freewheeling style, but still has a degree of control. Very few will just head to the airport and then decide where they are going, how long for, where they will stay and what will fill their time. Yet this is how some people seem to ‘fall’ into retirement. Planning ahead is essential to get the most out of the experience. Planning for, or reshaping, your retirement needn’t be dull or daunting if you think of it in the same terms as a ‘big trip’ where doing the research is great fun.

It seems that part of the problem is because people are not honouring their next life stage enough to set aside a few hours to think about where they are now, where they hope to be and – importantly – how they will get there.

Recent Vanguard Research underscores this lack of agency with findings that “despite rising retirement income expectations… almost one in two working Australians (48 per cent) have no plan for how they will prepare for retirement.”

Similarly, Retirement Essentials Retirement Pulse research found “57 per cent of respondents who are still working are concerned they will never have enough to retire in comfort.”

On this second point, many will be wrong. But until you do the hard yards and project your spending needs and likely income, you won’t have the relief of finding this out.

Goal setting isn’t for everyone, but taking some time think about your lifestyle priorities in retirement and what’s important to you is the first step. Make it a fun one. Choose a time when you won’t be interrupted, put on some background music, pour a wine, coffee or tea, and seat yourself in front of a blank sheet of paper.

Start with a very specific end in mind – if you are planning for a few decades, you will feel that you are guessing how long a piece of string is. Try a five-year window. What will less work and more play look like for you over a five-year period? Ask yourself:

These questions will help you become much clearer about your very specific needs (e.g. part-time work earnings, gym memberships, family loans, travel budgets). The more thoughtful you are in answering these questions, the easier it becomes to estimate how much you will need to spend each year to fund your lifestyle.

Your annual spending goal is the key to all good retirement plans so it pays to do the work to calculate how much you will need to be comfortable.

If you find this exercise far too difficult, you can review your current expenditure (say the last three months) and then consider which expenses will disappear when you leave full-time work and which extra expenses will need to be covered. That, too, will give you a picture of the type of income you’ll need.

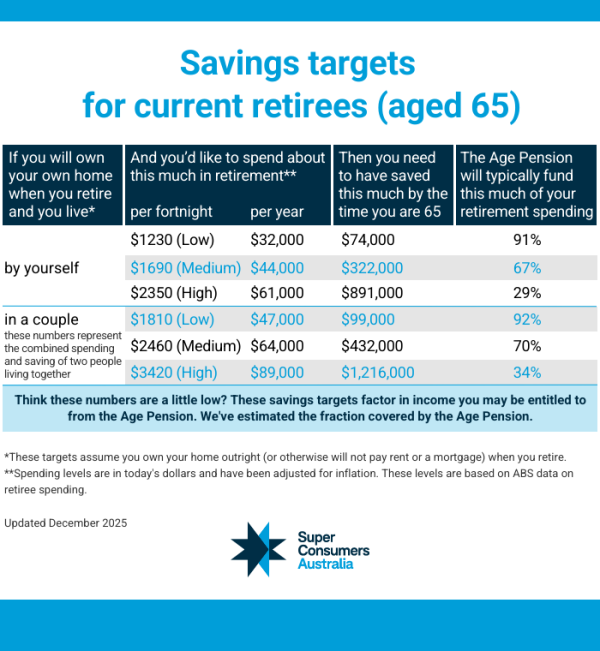

Alternatively, the following table is from advocacy group, Super Consumers Australia, with estimates of three different types of households and the size of budget they will require in retirement. This information is not definitive but does offer ballpark figures that many retirees find useful.

With a more clearly defined spending goal in mind, you can then go a step further to identify the different income sources that might combine to ensure your cash flow meets your spending target.

Typical sources include:

An alternative, increasingly popular source of back-up income is using the equity in your home. This could be through the government Home Equity Access Scheme (HEAS) or by using a reverse mortgage.

If you’ve followed the steps outlined above, we trust that you will now feel more confident about your likely income needs.

To see these strategies in action, let’s look at a real-life example. Retirement Essentials financial adviser Nicole Bell recently helped Carol find clarity through personalised projections.

Nicole to the rescue:

67-year-old Carol, working full-time but prefers to retire as soon as she can afford to. She is unclear how to project her needs.

The information shown on this website contains general information only and does not take account your specific objectives, financial situation needs or personal circumstances. You should seek personal advice or professional financial advice, consider your own circumstances and read our Product Disclosure Statement (PDS) before making a decision about Prime Super. A copy of the PDS and Target Market Determination is available by calling 1800 675 839 or by visiting primesuper.com.au/pds